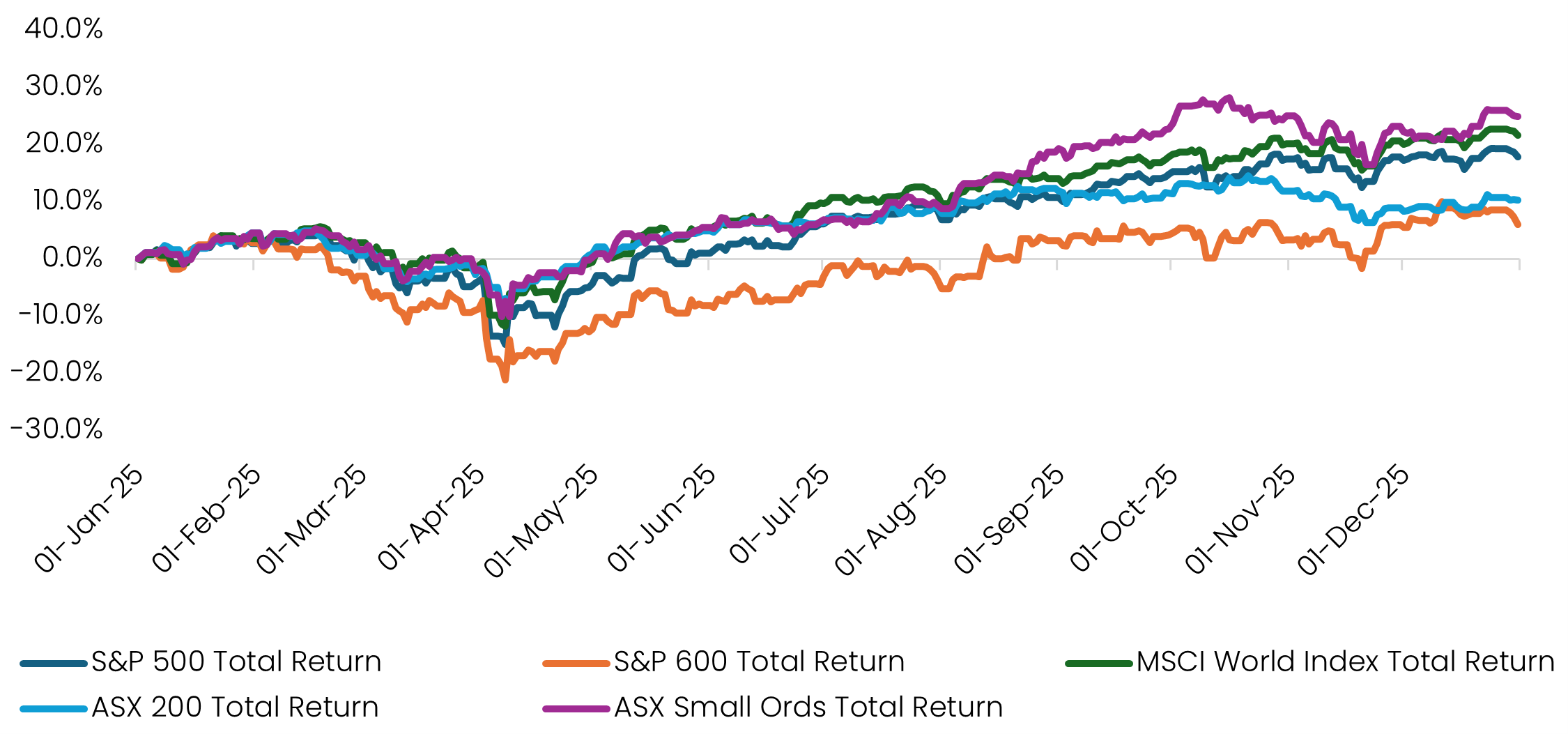

From a distance, 2025 may be observed as another strong year for investors, with global equity markets extending their post-pandemic run of gains. But the final results mask a year shaped by heightened uncertainty, abrupt market moves and a series of competing economic and geopolitical pressures that made the investment landscape anything but straightforward.

Source: S&P Global, Savana.

The year opened cautiously, as investors assessed the implications of a second Trump term in office. That caution turned swiftly to alarm in the second quarter, when the President’s tariff push triggered the sharpest market sell-off since the pandemic. The S&P 500 fell roughly 16% peak-to-trough, as fears around inflation, supply-chain disruption and global growth rapidly took hold.

With hindsight, the sell-off proved an overreaction. Markets once again underestimated Trump’s familiar playbook of brinkmanship and pragmatism. Initial “Liberation Day” posturing was soon followed by negotiated outcomes, including revised arrangements with the UK, Europe and Japan, alongside a tentative easing in tensions with China.

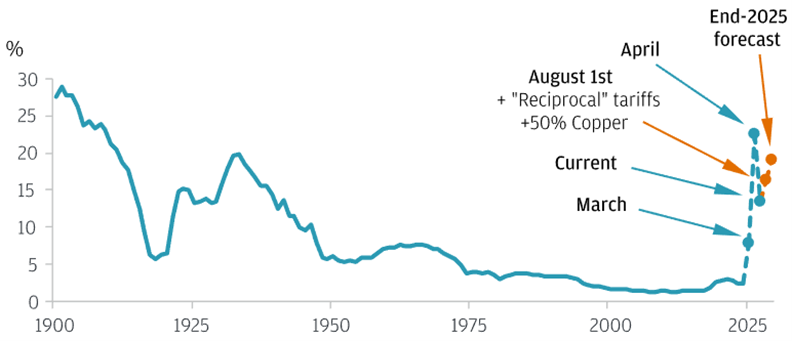

Source: JP Morgan. 2025. “US Tariffs: What’s the Impact on Global Trade and the Economy?” December 5, 2025.

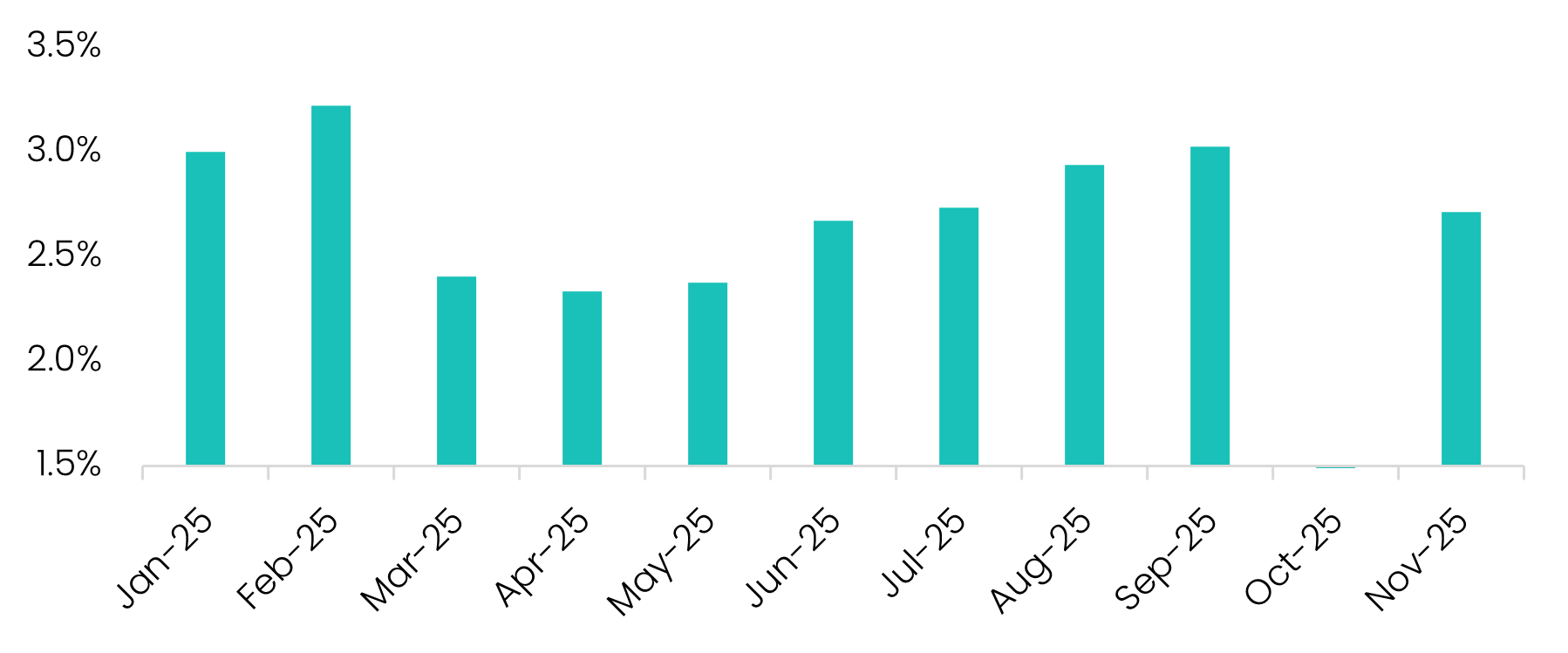

More importantly, the economic damage many feared failed to materialise. US inflation remained broadly contained - hovering in the 2.5–3.0% range, and sitting around 2.7% at the last count. Companies absorbed more of the tariff burden than expected, supply chains adjusted, and ongoing technology-driven productivity gains helped offset cost pressures.

Source: S&P Global, Savana.

For Savana, the episode reinforced three long-held principles: the importance of staying invested through periods of stress, the risks inherent in trying to trade around short-term macro noise, and the enduring robustness of the US economy despite adversity.

By mid-year, markets began to stabilise. The second half of 2025 saw a welcomed V-shaped recovery, as ever-plucky investors managed to shrug off lingering concerns around runaway fiscal deficits, geopolitical tensions and elevated valuations.

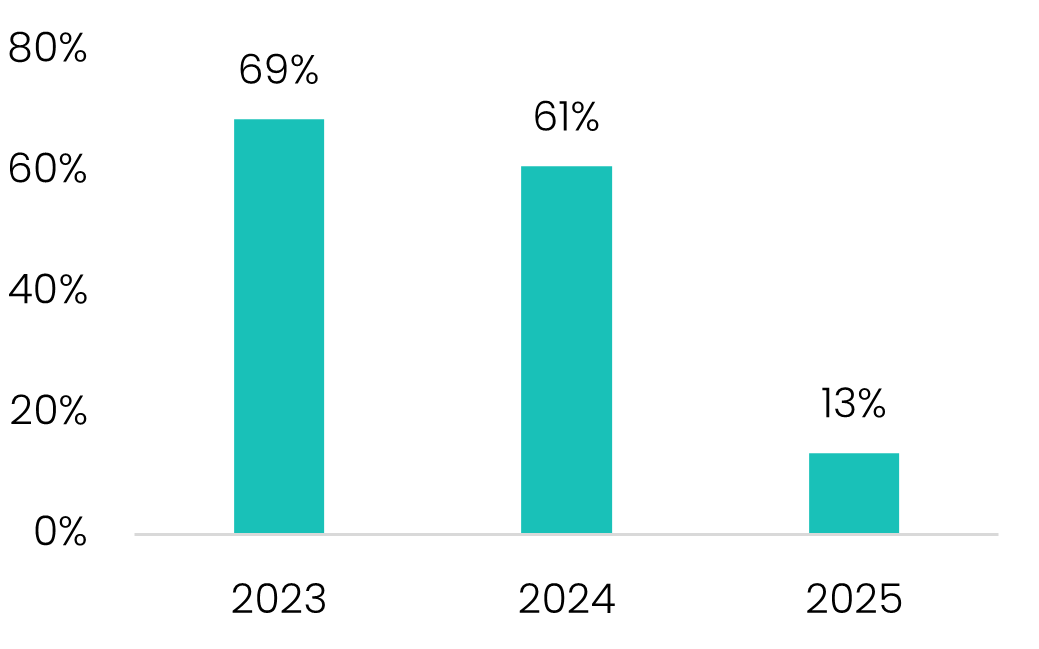

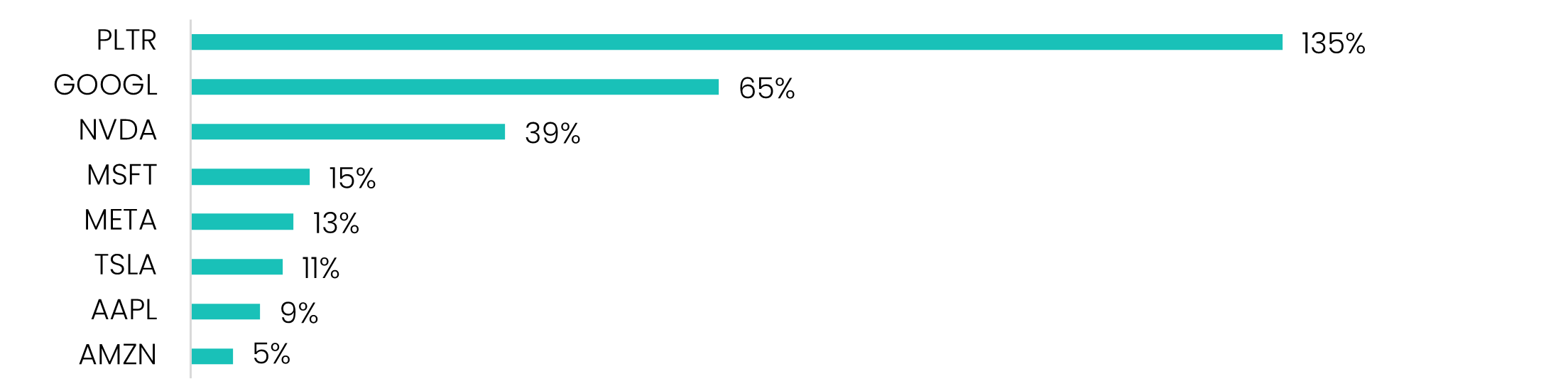

Optimism remained firmly anchored in Big Tech and the AI narrative. Despite slowing earnings growth and persistently stretched valuations, the Magnificent Seven – representing a third of the S&P 500 - collectively climbed a further 23%, led by standout gains in Nvidia (+39%) and Alphabet (+66%).

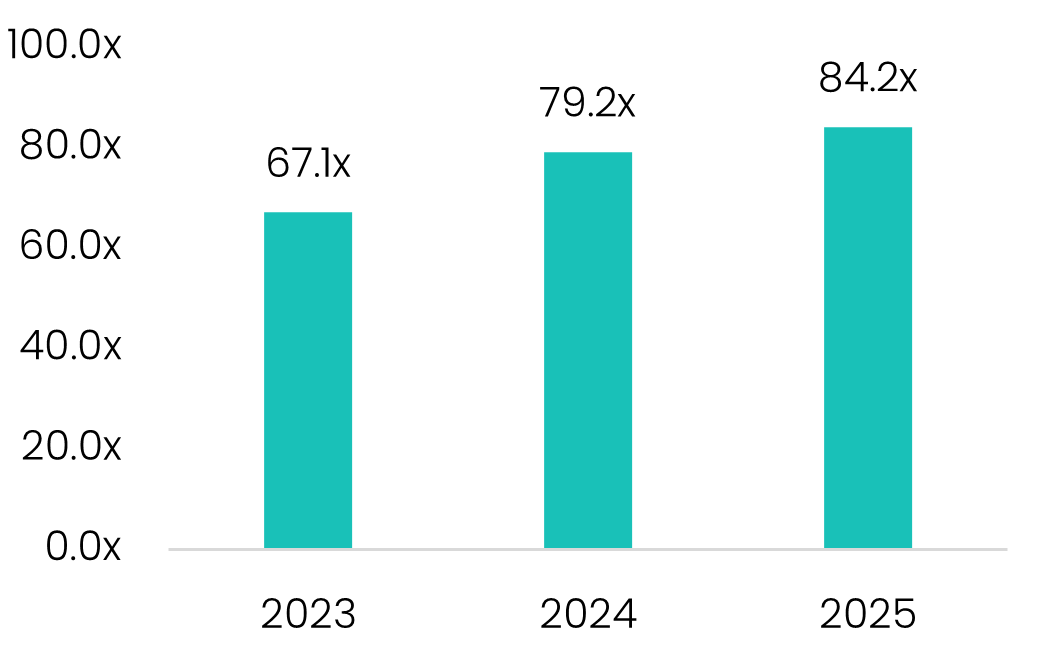

Yet the year’s biggest equity winner was big-data specialist Palantir, which surged 135% on the back of rapid revenue growth and its perceived leadership in applied AI. That rally, however, left Palantir with a less flattering distinction: one of the most expensive stocks in the S&P 500, with investors paying roughly $399 for every dollar of current earnings.

Source: S&P Global, Savana.

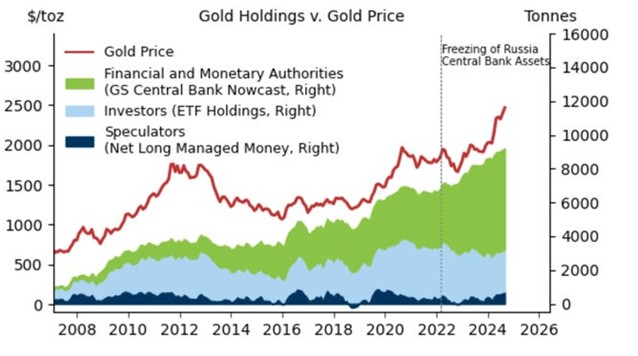

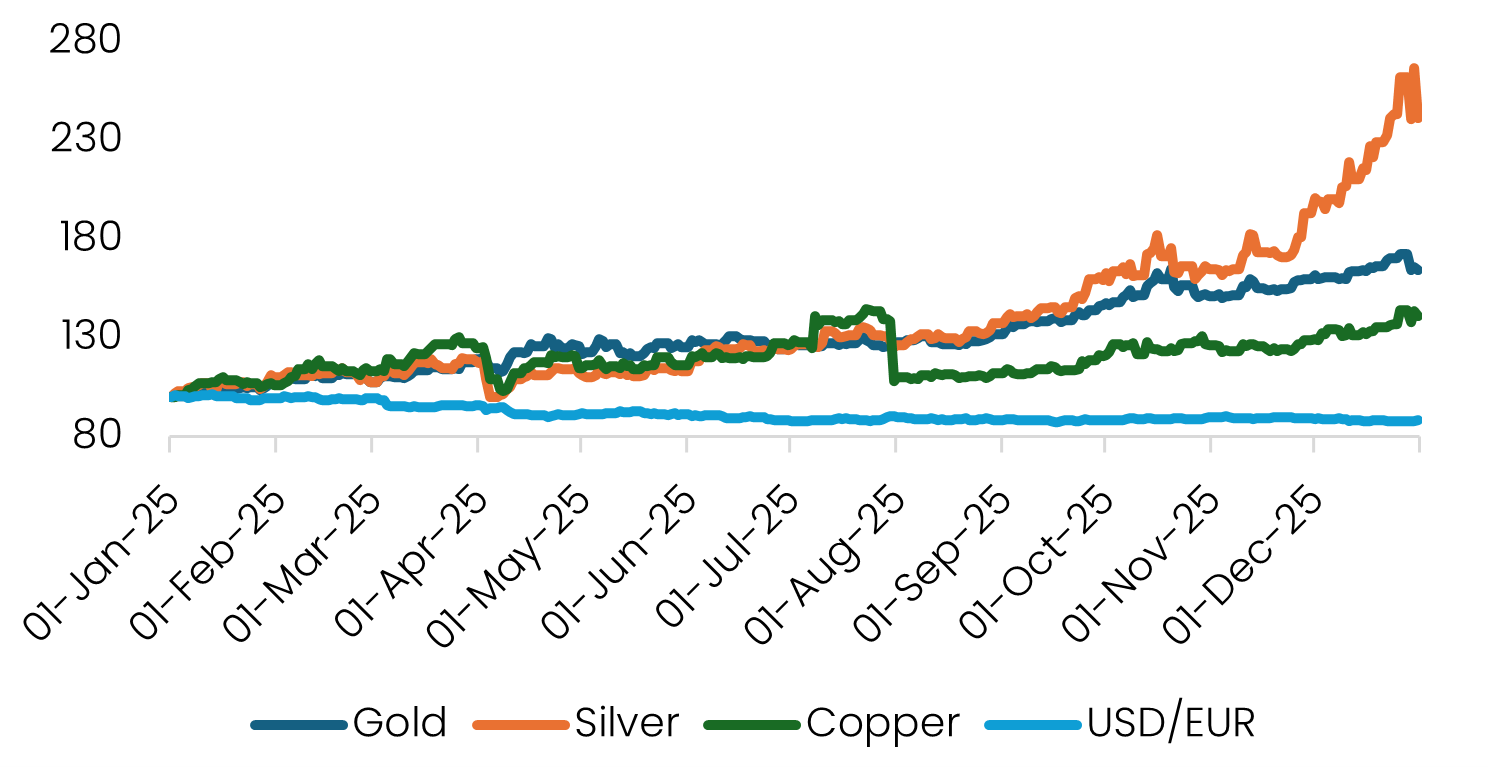

Away from equities, another defining feature of the year was the strong performance of commodities - particularly gold (+64%), silver (+141%) and copper (+41%). Silver and copper benefited from expanding industrial demand linked to renewable infrastructure, semiconductor equipment and defence.

Gold’s continued ascent, meanwhile, was widely viewed as a flight to safety amid inflation concerns, geopolitical conflict and market volatility. It also reflected a quieter structural shift underway. Central banks globally - most notably in China and Russia - continued to reduce their reliance on US dollar reserves by increasing allocations to gold.

This formed part of a broader shift away from US assets over the course of the year, driven by rising protectionism, fading enthusiasm for US exceptionalism and widening interest-rate differentials. The result was a notably weaker US dollar, down around 10% over the year.

Source: Goldman Sachs (via Business Insider, “3 reasons why surging gold prices will climb another 8% by the end of 2025, Goldman says”, November 1, 2024).

Source: S&P Global, Savana.

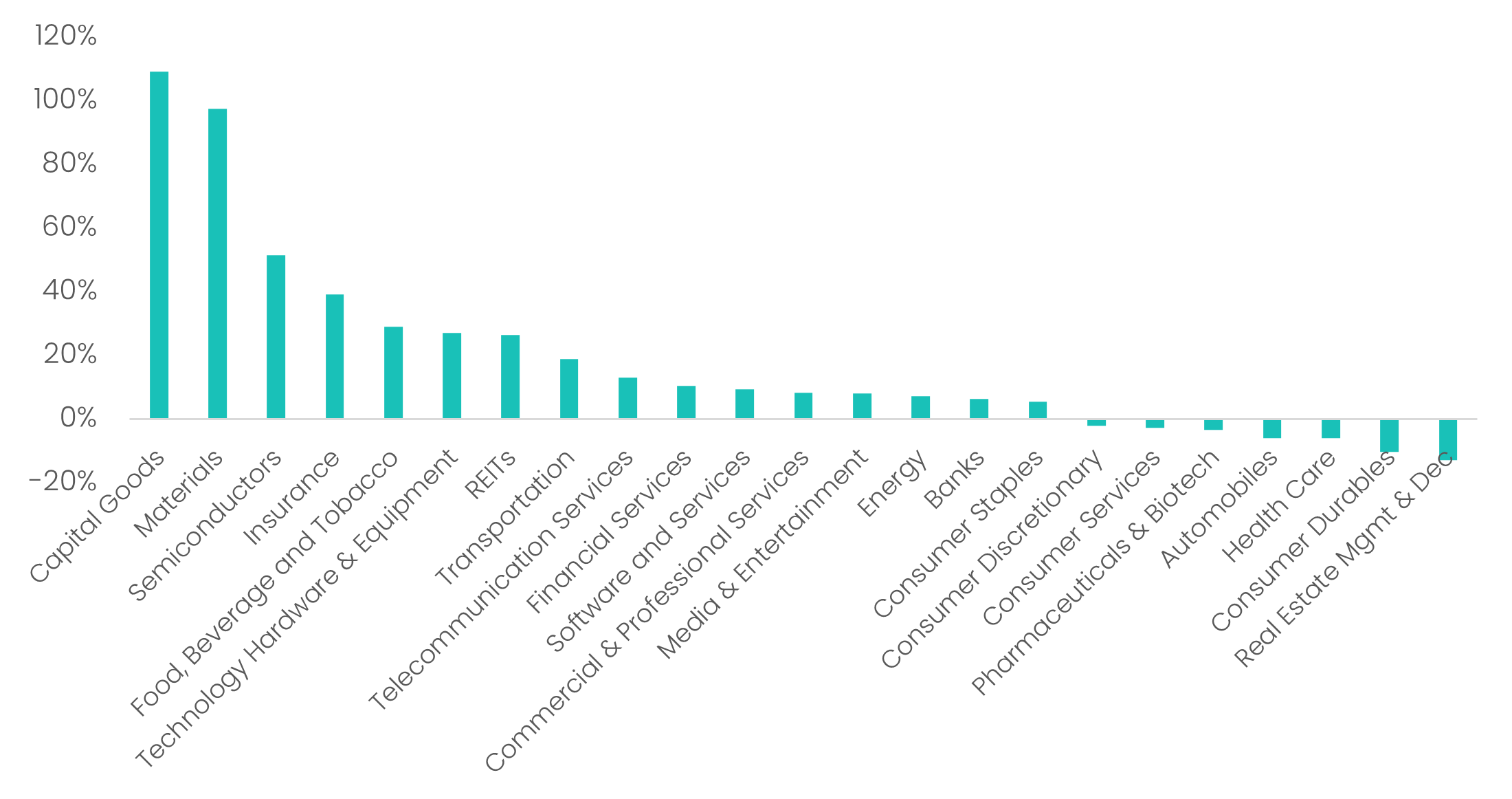

Closer to home, Australian equity markets also delivered a solid outcome. Of particular note was the renewed strength in the ASX Small Ordinaries Index (+25.0%), which outperformed the ASX 200 for only the second time in eight years.

While some attributed this to rotation away from large-cap defensives, the underlying driver was earnings growth of 34%. The result was powered by a high win rate (67%) and meaningful upside dispersion, with 25 of the 194 companies in the index delivering returns in excess of 100%.

Of those standout performers, 18 were specialist gold or diversified metals companies, while several Aerospace & Defence names also featured prominently - including Electro Optic Systems (+686%), DroneShield (+334%) and Austal (+133%).

Source: S&P Global, Savana.

Markets are never straightforward, but 2025 presented a particularly complex mix of extraordinary and often competing forces:

• Elevated valuations were traded-off against the transformative growth potential of AI.

• Large fiscal deficits helped keep economies moving, but at the cost of upward pressure on inflation and an ever-growing debt burden.

• Monetary policy was caught between competing demands on both sides of the dual mandate.

• Long-held notions of US exceptionalism were challenged by an unconventional and increasingly interventionist administration.

• And geopolitics continued to play a more prominent role, with US–Europe decoupling and a renewed push for national self-sufficiency supporting a shift in capital towards local markets.

For all its complexity, 2025 reinforced a familiar truth: clear strategy and disciplined execution tend to reward long-term investors. Savana’s systematic approach reflects this philosophy, grounded in the belief that attractively valued companies with strong fundamentals will deliver superior outcomes over time.

As for 2026, our only prediction is that elevated uncertainty and volatility are here to stay.

Good luck to all investors.

.png)