1. Valuation Decoded: Evidence That Markets Can Be Beaten - Systematically

2. CSIQ’s Time in the Sun: How a Simple Shift in Sentiment Delivered a 120% Bi-Monthly Return

3. Is the US Primed for Growth?: Deglobalization Could Lead to a Capex Boom Rivalled only by WW2

Earlier this month, we released our latest White Paper, Valuation Decoded, a deep-dive into the empirical foundations of Savana’s Collective Intelligence framework. The findings confirm what our philosophy has long asserted:

- Markets are efficient most of the time - but their mistakes are systematic, measurable, and exploitable.

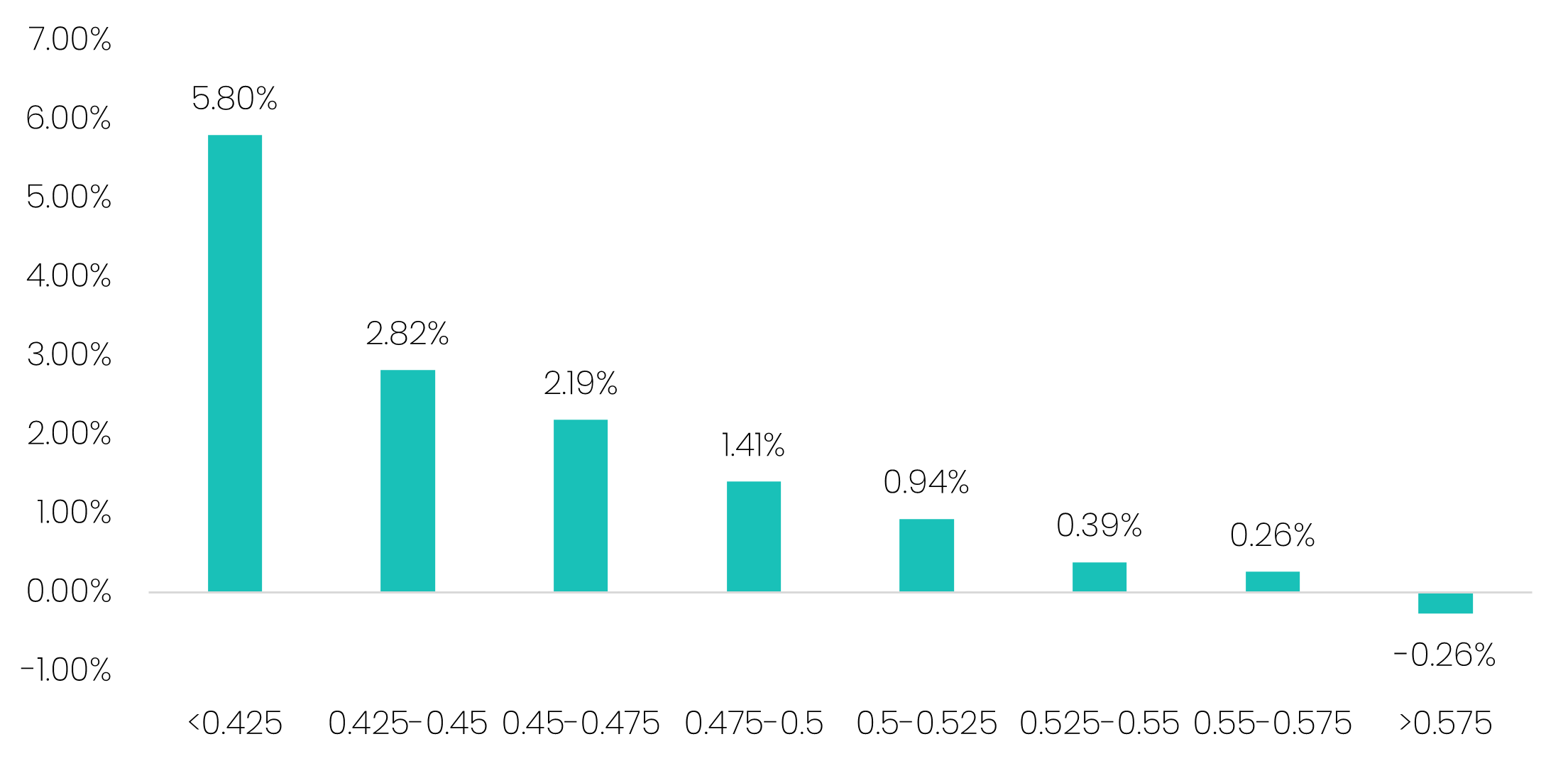

To test this thesis, we analysed 10 years of data spanning 145,000 company observations, measuring the relationship between Savana’s algorithmic valuations and subsequent two-month returns.

Source: S&P Global, Savana. Average bi-monthly returns by Savana’s valuation outputs, spanning all US-listed companies from 1-Jan-15 to 1-Jan-25. Companies are assigned a valuation score between 0 and 1, with 0.5 representing intrinsic fair value. Return distributions are winsorized (clipped) at the 1st and 99th percentiles to control for extreme outliers.

The results are striking. Companies identified by our model as undervalued outperformed those assessed as overvalued by an average of 6% in the following period. Moreover, the pattern is remarkably linear, with the chart showing a steady decline in bi-monthly returns as valuations increase. This is supported by regression analysis, which shows a negative slope of –0.0042 (p = 0.0013) with an R² of 0.84, confirming a powerful, statistically significant relationship.

This finding represents a major milestone for Savana. Having already observed persistent outperformance through back-testing and paper-trade portfolios over a long period of time, Valuation Decoded provides robust statistical validation that our algorithmic framework delivers a genuine and durable edge in long-term performance.

For investors, this is more than an academic achievement. It is the foundation of the Savana US Small Caps Active ETF (ASX: SVNP) - which applies the same Collective Intelligence framework daily to identify and capture mispricings in real time. By harnessing the predictive power of Savana’s model, SVNP gives investors direct access to a system engineered to exploit market inefficiency.

One of the big winners in the portfolio over the last two months has been Canadian Solar (NASDAQ: CSIQ) - a global leader in solar panel and battery-storage solutions.

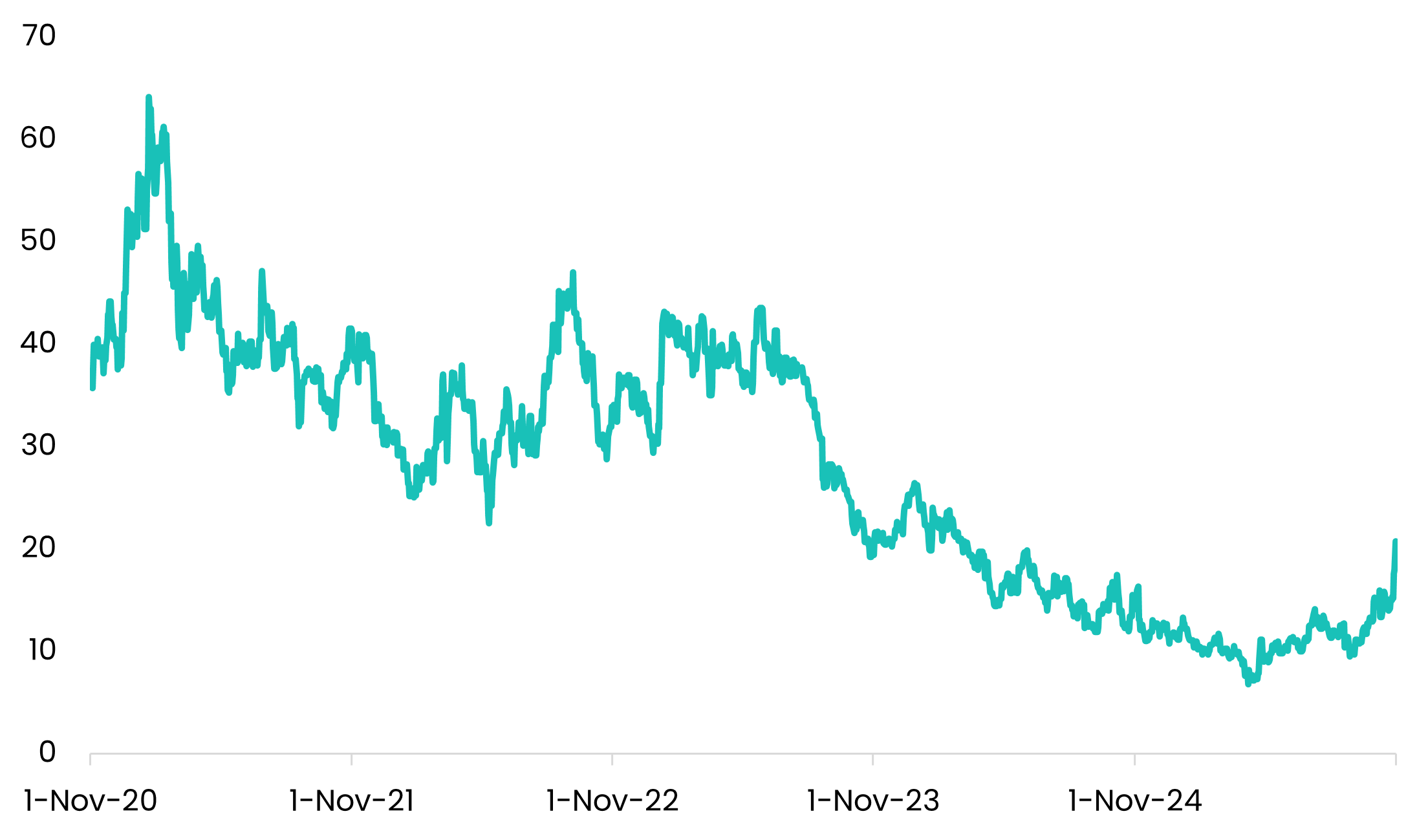

Since peaking in 2020, CSIQ’s share price has been locked in a near-four-year downtrend, falling more than 70% from its highs. Yet, beneath that chart, the company’s fundamentals have remained largely stable. In fact, revenue and net profit have actually increased by 70% and 16% respectively since December 2020.

The culprit behind the deteriorating share price, therefore, hasn’t been underlying business performance – but sentiment. The solar industry has been caught in a multi-year malaise, weighed down by geopolitical and overcapacity concerns in China, price compression, and investor fatigue after years of subsidy uncertainty.

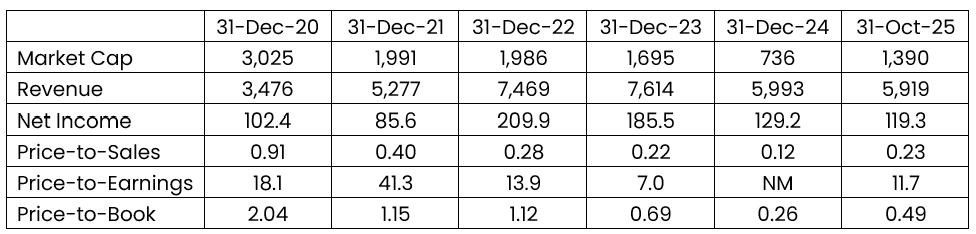

Some research houses had CSIQ trading at an ~80% discount to its sum-of-the-parts valuation. This is underscored by the fact that the value of CSIQ’s Shanghai-listed Chinese subsidiary alone (CSI Solar – of which CSIQ owns 62%) has a market cap worth ~3.5x the value of its parent.

Source: S&P Global.

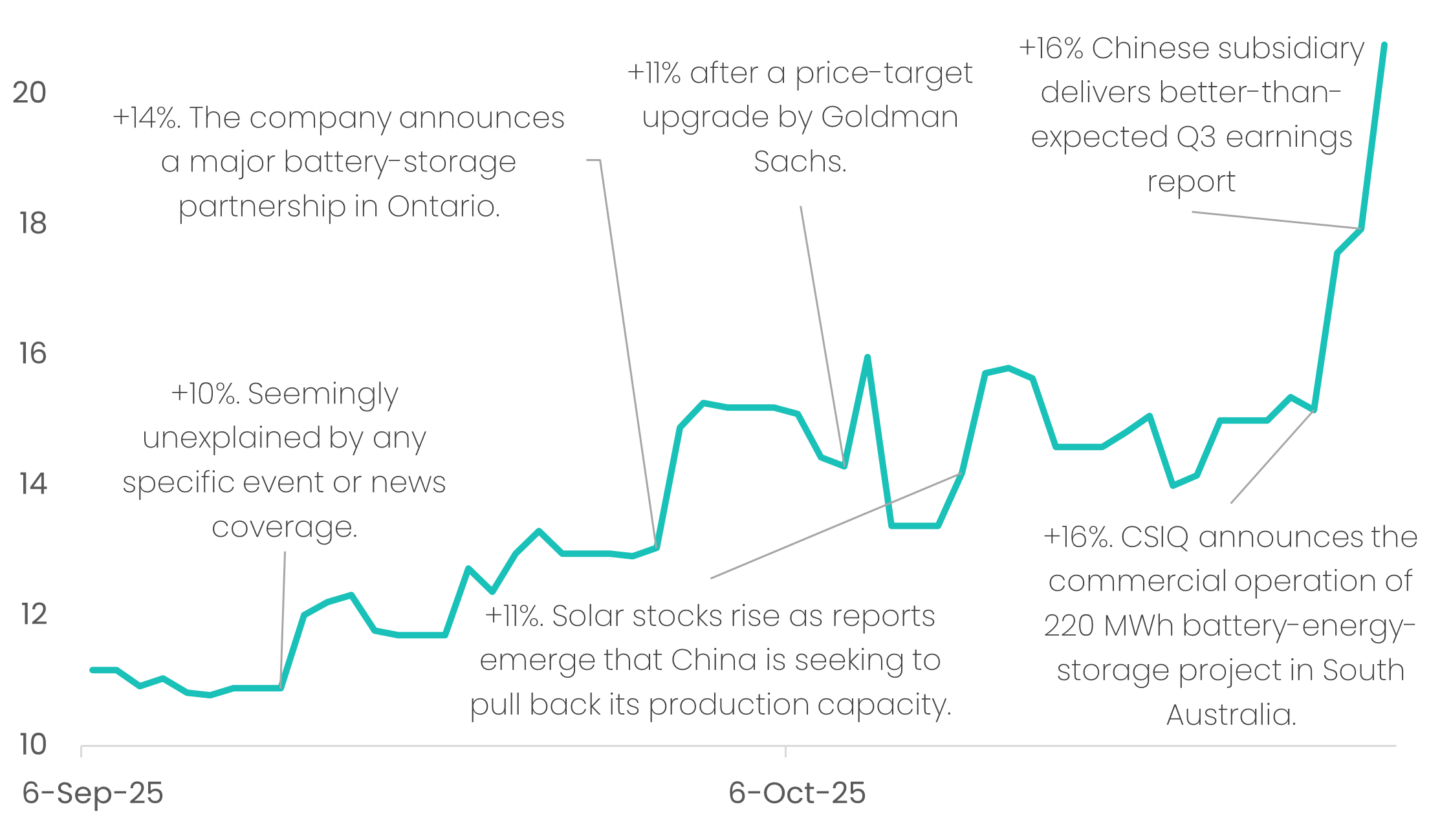

But sentiment is cyclical - and it can turn sharply. Over September and October, a combination of wave of favourable announcements and improving Chinese sector data have catalysed a powerful reversal. Canadian Solar has surged more than 120% in the last two months, rallying on renewed optimism around its energy-storage business and structural demand for clean-energy infrastructure.

Source: S&P Global. From 7-Sep-25 to 31-Oct-25.

For Savana, this is precisely the kind of opportunity our algorithm is designed to capture. Our valuation model systematically scans for companies whose valuations have detached from fundamentals. CSIQ was a textbook case: durable financials, deeply oversold, and sentiment poised to mean-revert.

Many of our best-performing holdings look like CSIQ at entry – companies with long-run price declines. To most investors, these are “falling knives” to be avoided. To us, they represent an asymmetric opportunity, where downside is limited and upside is magnified once sentiment normalises. Like Howard Marks says:

“It is our job as contrarians to catch falling knives, hopefully with care and skill. That’s why the concept of intrinsic value is so important. If we hold a view of value that enables us to buy when everyone else is selling – and if our view turns out to be right – that’s the route to the greatest rewards earned with the least risk.”

While fear and discomfort push most investors away, our algorithms consistently time entries near the point of maximum pessimism where prices bottom-out and a corrective rebound follows. In the case of CSIQ, we initiated the position on 7 September and are now preparing to exit in the 7 November rebalance, capturing an expected +120% gain in just two months.

A recent piece in the FT posed the question: is America sucking in growth from the rest of the world?1

It highlights a story that deserves more attention. There may just be logic behind the chaos of the tariff war. Now, before you choke on your latte, we have been following the trade war developments closely and the contrarian in us believes this deserves your attention.

The general consensus among economists is that the significant new tariffs imposed in 2025 have created a headwind for the US economy, leading to slower growth, higher inflation, and depressed business sentiment2 3. In short, post Liberation Day, American Exceptionalism died and, in its place, rose Gold and Emerging Markets.

This covers some of the truth but not the whole truth. It is certainly not all doom and gloom; on a relative basis the US is likely the cleanest shirt in the laundry. Why? The various US budget estimates generally exclude positive surprises such as tariff overcollections, trade deals and any peace deals in Ukraine or Middle East. The scale of capex being contemplated under Trump 2.0 alters the trajectory of the US economy and meaningfully improves debt to GDP.

This is because increased GDP growth comes without the concomitant increase in government spending. The rest of the world is funding US re-industrialisation and at the same time worsening their own growth prospects. In a high debt world, this relative improvement in the US fiscal trajectory matters, making USTs attractive and suppressing yields.

We recently calculated the total commitments and pledges since Trump 2.0 and found $12 trillion6 in total:

• Trade deals ($2.4 trillion),

• Middle East pledges ($3.2 trillion),

• Corporate re-shoring ($2.7 trillion),

• AI investment ($3.25 trillion), and

• NATO commitments to purchase ($0.7 trillion over next decade, excludes savings to US fiscus estimated at ~$3 trillion due to Allied spending)

This list is no doubt incomplete, and is unlikely to fully materialize; according to McKinsey only 2/3rds of FDI pledges become projects4. However, with trillion-dollar deals being bandied about, some will happen, and that is consequential to US growth and debt to GDP. The figures above exceed the World War 2 industrialization process of around ~$4-5 trillion in today’s terms, albeit on a smaller industrial base7.

If even $5 trillion materializes it could boost US GDP growth into the 2.5% - 4.0% range6, especially if the promise of AI productivity boost presents.

This is akin to a ‘Reverse Marshall Plan’ where obedience is enforced through restriction to the world’s largest consumer market. If other nations cannot find a substitute for the US market, the threat of further tariffs is credible and therefore the trade deal investment is credible. Reframing the US market under this context makes it a better investment destination than is currently believed and the near-shoring theme has longevity.

The global economy has entered a new regime defined not by economic optimization, but by geopolitical competition. The primary driver is a Cold War 2 between the US and China, with the US deploying a strategy termed the Reverse Marshall Plan. This strategy uses the strategic weaponization of US market access—primarily via tariffs—to coerce global capital into funding US national security goals: winning the AI race and re-industrializing its defense and tech supply chains.

China, especially under Xi Jinping, views its relationship with the West as a geopolitical and ideological struggle, aiming for technological self-sufficiency ("Made in China 2025," "dual circulation") and challenging US dominance. The effort is directly influenced by China's "Century of Humiliation," with leaders determined to avoid a repeat of that period of foreign exploitation and domestic weakness. Whilst complete autarky seems unlikely, any détente is likely a pause to shift reliance away from the adversary.

The question is who has the stronger hand? US consumer represents roughly a 1/3rd of global consumption5. It is particularly difficult to mitigate against it. Hence, the US are generally better positioned to prevail and secure the trade deal investment it desires.

Yes, China controls rare earths, but find another consumer market that can rival the US and wants to substitute the US knowing that trade with China means de-industrialization?

We find ourselves here today because China followed a state subsidised industrial policy based not on comparative advantage but on state driven goals such as Made In China 2025. The US sees itself pushing back against decades of what it now views as Chinese economic aggression – IP theft, forced tech transfer, state subsidies, and the disregard for WTO rules.

Many see this as the beginning of the ‘great decoupling’, with supply chain re-alignment expected to take years and possibly decades to complete. For Savana’s US Small Caps Fund, surprises to US GDP growth as contemplated – US$ trillions - will likely spillover from narrow growth to broader based. There will also be firms providing the picks and shovels for the rebuild that will benefit from increased demand.

As evidenced by one of Savana’s holdings, Fluor, which we see as a core 'picks and shovels' holding for this very theme. As a premier Engineering, Procurement, and Construction (EPC) firm, Fluor is one of the few global companies with the scale and technical expertise to actually build the complex semiconductor fabs, advanced pharmaceutical plants, and energy infrastructure at the heart of the re-shoring trend. To quote POTUS, this is merely the start of something much bigger and more beautiful.

1. https://www.ft.com/content/4c6efb87-9d65-4d31-8198-9a8e9be2cc34

2. https://www.jpmorgan.com/insights/global-research/current-events/us-tariffs

3. https://www.conference-board.org/research/us-forecast

4. https://www.mckinsey.com/mgi/our-research/the-fdi-shake-up-how-foreign-direct-investment-today-may-shape-industry-and-trade-tomorrow

5. https://worldpopulationreview.com/country-rankings/consumer-spending-by-country

6. $12 trillion dollar estimate sourced internally by Savana from various sources. GDP growth forecasts are based on CBO base case with positive surprises included based on ~$5 of the $12 trillion estimate materializing over the next decade.

a. https://www.whitehouse.gov/articles/2025/08/trump-effect-a-running-list-of-new-u-s-investment-in-president-trumps-second-term/

7. https://online.norwich.edu/online/about/resource-library/cost-us-wars-then-and-now#:~:text=Though%20it%20lasted%20fewer%20than,gross%20domestic%20product%20(GDP).