Most active managers start with the premise that the market is wrong, and they know better. We think that is backwards. The more useful starting point, and the one that we have been researching for the better part of a decade, is that the market is usually right, that this is no accident, and that understanding precisely why it is right tells you where and when it is likely to be wrong.

The reason markets are so hard to beat is not mysterious. It is the same reason a crowd at a country fair can guess the weight of an ox more accurately than the prize cattle judge, the example Francis Galton documented in 1907. The stock market is a crowd of the same kind, only vastly larger. Millions of participants, each with their own information, methods and biases, buy and sell in response to new information. Those independent judgements aggregate into a single price, and the errors in them, the optimism of one, the pessimism of another, tend to cancel. What survives is something close to fair value. This is the mechanism beneath the Efficient Market Hypothesis, and it works.

What is less widely appreciated is that this accuracy is not a permanent property of markets. It is a conditional one. And that condition can be written down as a simple equation.

Most active managers start with the premise that the market is wrong, and they know better. We think that is backwards. The more useful starting point, and the one that we have been researching for the better part of a decade, is that the market is usually right, that this is no accident, and that understanding precisely why it is right tells you where and when it is likely to be wrong.

The reason markets are so hard to beat is not mysterious. It is the same reason a crowd at a country fair can guess the weight of an ox more accurately than the prize cattle judge, the example Francis Galton documented in 1907. The stock market is a crowd of the same kind, only vastly larger. Millions of participants, each with their own information, methods and biases, buy and sell in response to new information. Those independent judgements aggregate into a single price, and the errors in them, the optimism of one, the pessimism of another, tend to cancel. What survives is something close to fair value. This is the mechanism beneath the Efficient Market Hypothesis, and it works.

What is less widely appreciated is that this accuracy is not a permanent property of markets. It is a conditional one. And that condition can be written down as a simple equation.

The maths of a wise crowd

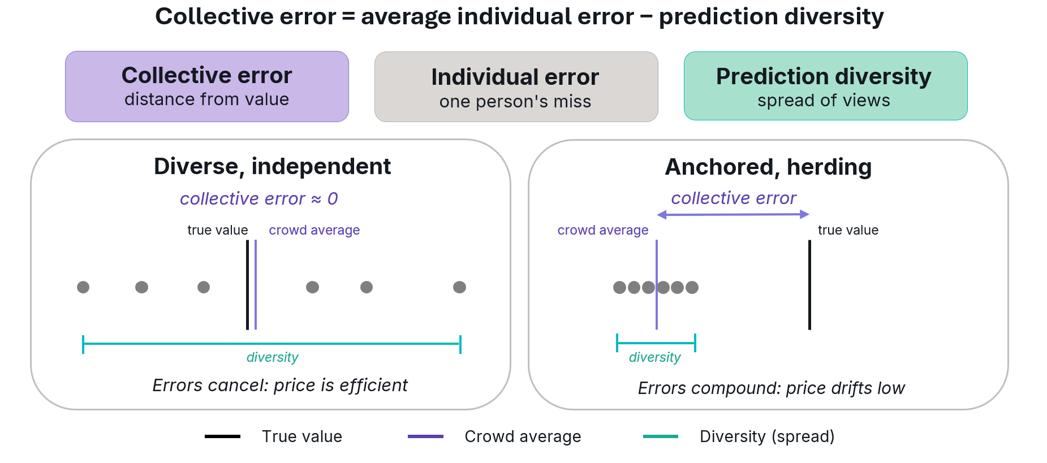

In 2007 the University of Michigan and Santa Fe Institute complexity scientist Scott E. Page formalised the wisdom of crowds into a mathematical identity he called the Diversity Prediction Theorem. It states that a group’s collective error equals the average error of its individual members minus the diversity of their predictions. Page writes it simply: collective error equals average individual error minus prediction diversity. The implication is profound and slightly counterintuitive. A crowd’s accuracy does not come only from the skill of its members. It comes, in equal measure, from how much they disagree. Diversity is not a nice-to-have that makes a group feel balanced. It is a critical condition for ensuring accurate decision making.

Page’s larger body of work, summarised in The Difference (2007), makes the point sharper still. He argues that the strength of a crowd lies in what he calls many-model thinking: the fact that different people bring different perspectives and genuinely different ways of interpreting the same problem. One investor looks at cash flows, another at price momentum, another at industry structure, and another at sentiment. Because their models and their thinking are different, their errors point in different directions, and the disagreement itself does the work of cancelling those errors out. As Page puts it, when a problem is hard, you are better off listening to people who think differently from you, even when they are individually less accurate. It is the variety of the models, not the brilliance of any one model, that produces the wise result.

Diversity Prediction Theorem in Action

Efficiency is a condition, not a constant

This reframes market efficiency in a way we find far more useful than the textbook version. Efficiency is not a switch that is permanently on. It is an emergent property of a system that happens, most of the time, to satisfy two conditions: a genuine diversity of independent views, and enough of them. When those conditions hold, prices are accurate and the market deserves the deference passive investing pays it. The corollary is the part that matters. When either condition weakens, the theorem says the collective error must rise. Efficiency degrades not because participants become foolish, but because their judgements stop being independent and their models stop being diverse. The disagreement that was doing the work disappears, and price drifts away from value.

Markets supply no shortage of examples. Herding, feedback loops and the familiar oscillation between fear and greed all do the same thing in the language of the theorem: they collapse diversity by making everyone’s errors point the same way. Correlated error is the enemy of an accurate crowd, and the conditions that produce it are not evenly spread across a market. They cluster.

Where the gaps appear

This is where the abstract becomes practical. If the wisdom of a crowd depends on the diversity and independence of its participants, then the parts of the market with the deepest, most varied and most independent participation should be the most efficiently priced, and the parts where participation is thin, correlated or narrative-driven should be the least. The largest companies in the world are followed by thousands of analysts and investors applying every conceivable model. That crowd is enormous and diverse, and the theorem says it should be accurate. We agree. Our research shows that the largest companies tend to almost always we fairly valued, and the concentration of capital into them is not the same thing as their price being wrong.

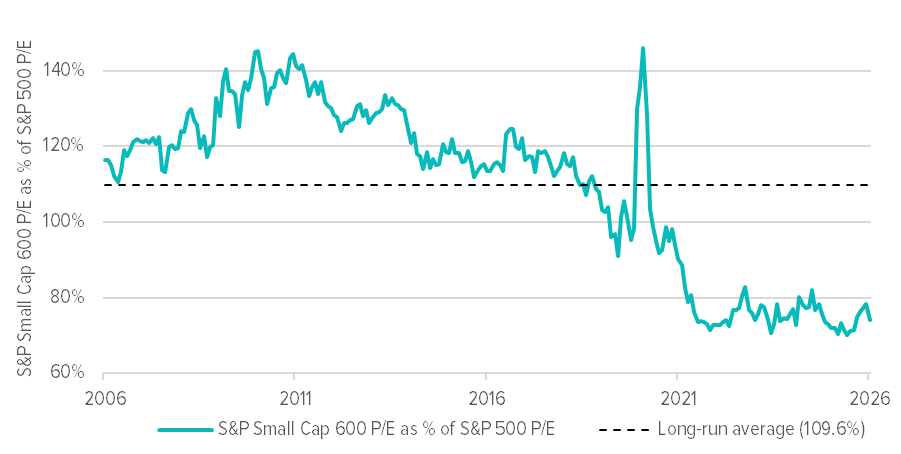

The opportunity sits at the other end. In the neglected corners of the market, where fewer participants are watching, where a single story can dominate what little attention there is, the diversity term in Page’s identity is small, and collective error is correspondingly larger. This describes the market for small caps almost perfectly. Looking at the US market specifically, small caps currently trade at one of the widest valuation discounts to large caps in more than two decades, by some measures their cheapest relative position since the late 1990s, and as a share of the total US market they have shrunk to around 5 per cent against a long-run average closer to 8 per cent. None of that guarantees a near-term rebound. But it is precisely the environment the theorem predicts will be inefficiently priced, and therefore precisely where disciplined security selection can uncover opportunities to outperform.

Relative Valuations of Small and Large Cap Shares

How we put this to work

This is the science Savana is built on. We do not try to outsmart the crowd, because most of the time it cannot be outsmarted. We study it. Our work is to identify, systematically and without sentiment, the specific moments and segments where diversity and independence have eroded, where the theorem says the crowd has stopped being wise, and to act where the distance between price and fair value is widest. In a market as broad as the US, those gaps are not hard to locate. They are simply unfashionable, and in our experience unfashionable is usually where the work pays off.